Are you thinking about refinancing your auto loan? Here are some things to consider to help you decide if refinancing is the best option for you.

How does auto loan refinancing work?

When you refinance a car, you pay off your current loan with proceeds from new loan with a different lending company. The loan terms can remain the same or change, depending on the desired outcome. For more details, give us a call and ask to speak to a loan officer.

Why refinance my auto loan?

People commonly refinance their auto loans to save money, as refinancing could get you a lower interest rate. As a result, it could decrease your monthly payment.

If you can’t find a better rate, you may be able to find another loan with a longer repayment period, which might also result in a lower monthly payment (although it might increase your total interest cost over the life of the loan).

Let’s look at the pros and cons of refinancing your auto loan.

Pros

- Lower Your Interest Rate

If your credit score has improved since taking out your auto loan, you may be able to get a new loan with a lower interest rate. When you lower your interest rate you may reduce the total interest charges you pay on your car loan – assuming your car loan term is not extended or not extended by too many months. - Lower Your Monthly Payment

Refinancing might allow you to extend the loan term, which will then lower your monthly payment. Keep in mind you might end up paying more interest over the total life of the loan.

Cons

- Fees

There are a variety of fees you might run into including a prepayment penalty or origination fees. When comparing your refinancing options, be sure to ask about what fees will be charged, if any. Service First does not charge any loan origination fees or assess any prepayment penalties on auto loans. - Paying More Interest

While getting a lower interest rate can save you money, if you extend the term of the loan you might pay more interest over the life of the loan.

Example

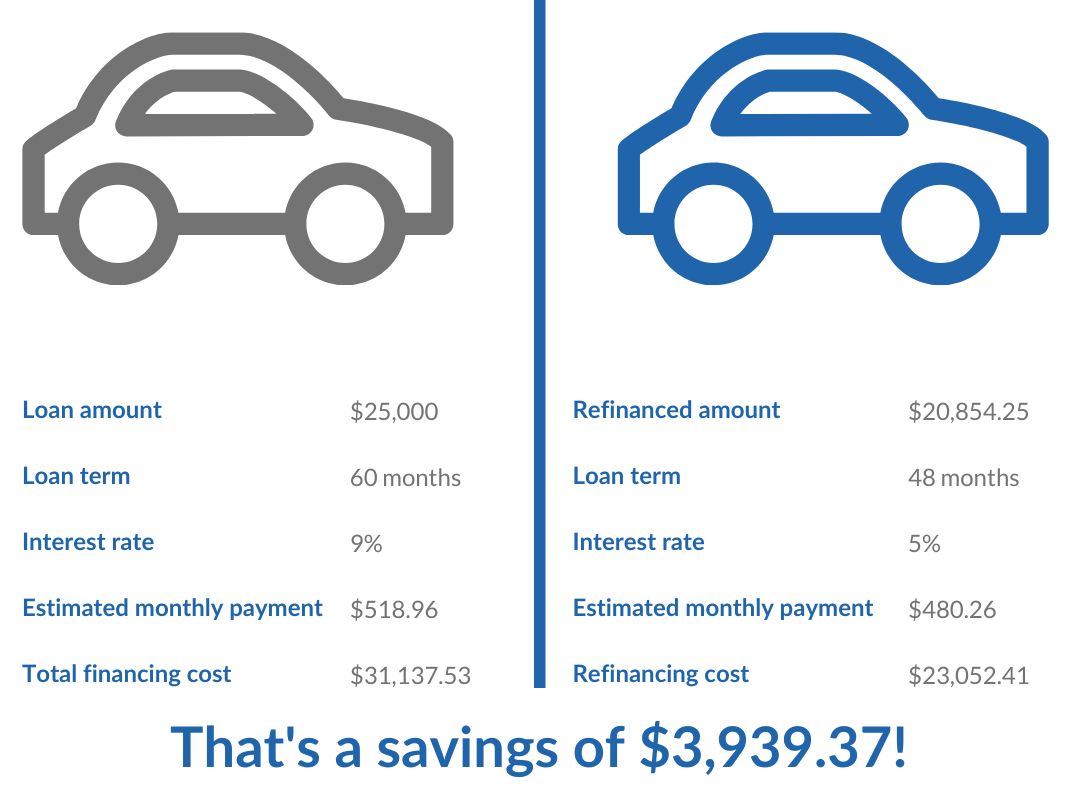

Let’s say your original auto loan was for $25,000, with a 9% interest rate and loan term of 60 months. After a year of payments on this loan, your balance is now $20,854.25. If you keep this loan for 60 months, you’ll end up paying a total of $31,137.53. If you were to refinance and get a loan for $20,854.25 for the remaining 48 months with a lower interest rate of 5%, you’d end up paying a total of $23,052.41 on your refinanced loan. Combined with the $4,145.75 you paid on the previous loan, you’d have paid a total of $27,198.16 to finance your car — $3,939.37 less than if you had kept your original loan.

You can use our auto refinance calculator and enter in your own loan numbers to get a customized report.

When it comes to refinancing your auto loan, you should compare the pros and cons and make an informed decision. To learn more about refinancing an auto loan with Service First, check out our Switch & Save offer. Bring your current loan over and we’ll match or beat the rate by up to 1% APR! Plus there’s no application or origination fee.